But, we get it. Just because it’s happening to a lot of people doesn’t necessarily make you feel better. Let’s dive into the “why” behind these increases, so you can stay in-the-know.

Let’s begin with home insurance.

Accumulated claim history throughout the market plays a role in the increase of home insurance premiums along with severe weather events, labor shortages and the increased cost of building materials. Weather events were anything but quiet in 2023. The National Oceanic and Atmospheric Administration (NOAA) estimates that 28 weather disasters occurred in the U.S. through August 2023 with damage of at least $1 billion each.

Labor shortages in the construction industry are another factor. Without enough workers, it can take much longer to repair or replace a home, which can contribute to higher claim costs.

So, what about auto insurance?

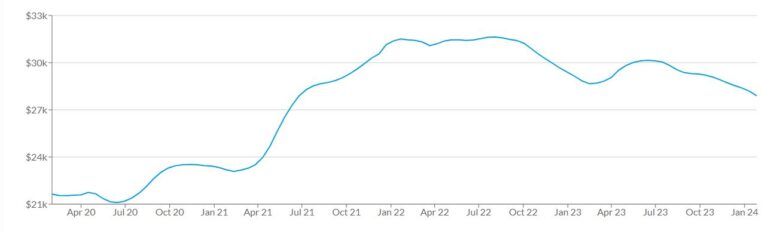

Like home, claim history also impacts the rise of auto insurance premiums. The cost to settle claims has increased drastically due to supply and labor shortages and used vehicle market values. The longer it takes for supplies to arrive, the longer insurance companies must pay for the extended waiting period, especially for coverages like Additional Expense, which provides rental car coverage (subject to the applicable limits of rental insurance). All of these factors combined might result in higher premiums.

Used Vehicle Market Values pre-Covid to today. CarGurus.com

Rate increases can be frustrating, especially if you’ve never filed a claim.

But, the reality is that market forces such as deflation and inflation also impact the costs to repair or replace covered property. While other carriers are responding to these challenges by closing their doors to new business, our doors remain open.

While costs to repair or replace covered property generally do not decrease, your local, independent insurance agent can help you set the appropriate limit for your home or vehicle in the event of market changes.

Many of the increases you might see are uncontrollable since they are a response to changes in the market. However, there are a few things that you can control to potentially limit the severity of a possible loss.

On the home insurance side of things, unfortunately, we can’t control the cost of labor or mother nature’s impact.

Here are some things you can do to potentially limit the severity of a loss:

- Proper winterizing of seasonal or secondary homes

- Regular home maintenance

- Roof inspections

For auto insurance, you can control your driving habits. To limit the severity of an accident or prevent it completely, practice safer driving habits.

- Proper hand placement on wheel

- Defensive driving

- Undistracted driving

These risk limiting measures may not equate to an immediate premium reduction. However, they may reduce the cost of the repairs in the event of a loss.

We know it’s hard to see your insurance premiums go up. Hopefully, by understanding the “why” behind these increases, you feel more informed. After all, you are not alone; market changes impact many people. For more information about the rate increases, reach out to your local, independent insurance agent today.